I've come up with a way to keep track of and budget my money. I'd like to share what I have - perhaps some of my suggestions will be helpful. Before reading through this, ask yourself how detailed you want to be -- not all of the following steps may be needed for your purposes.

Step 1: Create a Template Spreadsheet.

If you want a copy of my spreadsheet rather than make one from scratch just get in contact with me.

You can use Microsoft Excel or a similar program; whatever you're more comfortable with. I used Excel so the following instructions will be for this program.

The first chart should look like this:

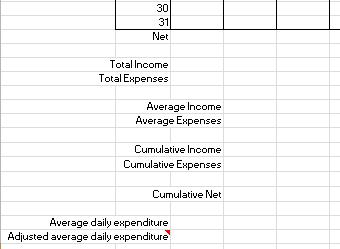

Input the year at the top, 31 days at the left, and the 12 months at the top.

Underneath this chart, include the following:

I'll explain this set-up later, but first let's finish the template. There are 3 sub-sections you can include:

I) Limits

II) Money Pools

III) Accounting

Save your template and you can reuse it each year.

Step 2: Daily Tracking.

To do this it will be important to either save your receipts, makes notes on paper, and/or make notes on your iphone/blackberry/tablet/whatever device you have. At the end of the day, take out your receipts/notes and enter the sum into the appropriate cell of the main chart. (You can discard your receipts/notes afterwards). If you don't know the exact amount, you could make an estimate of what you spent.

If you have any income for that day be sure to include that and you could highlight the cells with income in green (this will make things easier later).

I've included 31 days, the maximum for any month, but some months have fewer days. For those extra days just enter zeros.

Personally, I've only used this template while I had income but even when you don't have any income you should make a habit of keeping track of your money. Once it becomes a habit, your mistakes will be fewer and this will allow for more accurate accounting.

Step 3: Monthly Tallying.

At the end of the month, tally up the sum of each cell in the column for that month - that gives you your net. For the total income, go back to the cells you highlighted and calculate the total. For the total expenses, take a shortcut and calculate it as follows:

total expenses = net - total income

You can then calculate the average income and average expenses for all of the months you have accounted for in that year so far. Calculate cumulative income using the sum of the cells in the "total income" row; similarly, calculate the cumulative expenses using the sum of the cells in the "total expenses" row.

cumulative net = cumulative income - cumulative expenses

Average daily expenditure can be calculated by dividing the total expenses by the number of days in that month. If you want, you can also do an adjusted average daily expenditure by removing unavoidable expenses.

Step 4: Money Pools.

I've created sections for Debit, Credit Card (Visa), cash on hand, and gift money. You can edit this (add in or remove sections) based on what you have. Count up your money in each section (i.e. check your bank account, count the money in your wallet) and then calculate the total money you have at the end of the month.

Gift money: I wasn't quite sure what to do with this, so I included a section underneath where you can tally up any gift money you received that month (this is a part of daily tracking actually). Gift money could be what people give you for your birthday or winnings from the lottery/gambling/other; basically anything you don't have to pay back. (If you want you could consider this as income and include it in the main chart but this could make it more difficult to budget your money - see step 6, part v).

Discrepancy: the sum of your previous month's total money (A) plus the net for the current month (B) plus gift money (C) should equal the total of your current money for that month (D). If not then there is a discrepancy.

discrepancy = A+B+C-D

There can be a few reasons for this:

-your calculations may be wrong - check this first

-a negative discrepancy (using the above equation) could mean your calculations are off or that your accounting is off; it seems unlikely that someone would be furtively slipping you money without making you aware of it

-a positive discrepancy could mean that you have excluded some expenses, or that someone has taken or is taking your money. This is where it is helpful to be accurate with your daily tracking as it can tip you off to the fact that someone is stealing money from you.

(Note: you can change the above equation to discrepancy = D-A-B-C which would reverse the above two points; do the calculation whichever way you prefer but be consistent).

Step 5: Accounting.

As you do your daily tracking you can leave comments in the cells giving a breakdown of where your money went according to different categories.

ex: cell: -$135.75, comment: $65.5 groceries, $26.76 other (clock), $5.99 extra (cap), $12.97 other (gel insoles), $24.51 extra (notepad, scissors)

Note: you don't have to be specific and include the things in brackets; using general categories may be detailed enough for your purposes.

At the end of the month you calculate a total for each category and include it in a chart (see Step 1 subsection III). I've included categories for rent/mortgage, student loans, groceries/food, gas/travel, and cell phone bill. You can remove categories if they aren't relevant and add other categories that are relevant (ex: other bills, prescription medications). I'll explain the bottom 3 categories:

Other: anything that is necessary/needed but doesn't fit the other categories. Ex: gifts, a pair of workboots for work, fixing unexpected damage, clothes.

Extra: anything that is unnecessary. This will vary depending on where you live and what your culture is. For example, internet connection may be considered necessary, cable tv may be considered necessary, alcohol may be considered unnecessary. Whatever you decide, try to be consistent.

Unclassified: anything for which you forgot to include a comment as to which category this expense belongs to. Ideally this section should be zero.

Accounting in this way will give you a breakdown of where your money is going. Depending on how detailed you want to be, you could just omit step 5 altogether or you could go a step further and create pie charts to give you nice visual representations like so:

Step 6: Budgeting.

Accounting was when you kept track of your money and where it was spent. With budgeting you can set limits on your spending, set goals for how you want to spend your money, and set a goal for how much of your income you want/need to save. There is one basic rule you should go by:

The sum total of your income should be greater than or equal to the sum total of your expenses.

Spending more than you earn is not sustainable. Spending an equal amount as you earn is sustainable but it is a no growth situation. You should try to save some money each month. With that in mind, I've made up a few rules/suggestions to go by:

i) Have "buffer money" for unexpected expenses. Save 10% of income every month.

ii) Set daily or weekly limits on how much you can spend. Here's a formula you can use:

Weekly Limit = [(1-z)(income) - (unavoidable expenses)](7/days in month)

z is the percentage you want to save including the percentage for buffer money. Personally, I would go with 30%, so I would enter 0.3 into the above equation.

I subtract unavoidable expenses (ex: bills, student loans), so I get an idea of how much extra money I have that I can freely spend.

You could also go by a daily limit but there will be fluctuations in your spending so it may be simpler to go with a weekly limit. Overall, you should aim to meet or surpass the limit (i.e. spend no more than the limit).

iii) When calculating the weekly limit use the average income of past months and round down to the nearest 100.

If you don't have an average income to go by then you'll have to make an educated guess. Keep in mind that it's better to underestimate your income than overestimate as the extra money you get will still be there to spend later.

iv) If a week overlaps two months then use the daily limits of the respective months for those days.

v) Do not include gift money when budgeting. If you included gift money in your income then that is an unreliable source as you can't expect to get a similar amount of gift money the next month - this would make your limits too loose.

Step 7: Evaluating Your Budget.

This is something you should do at the end of each week and month. For that, I've come up with an equation to check your conformity to your limits:

conformity = (weekly limit) - (sum of expenses for that week)

Note: exclude unavoidable expenses.

If you limits are too loose or stringent then you can re-adjust them as long as you follow the rule that the sum total of your income should be greater than or equal to the sum total of your expenses.

One other thing you can do is calculate how much money you have saved, which can simply be calculated by dividing your net for that month by the income for that month and multiply by 100 to put it as a percentage. Having this percentage will give you an idea of how effective your limits are, and you can use this to re-adjust your limits using the equation above in step 6.

Other Considerations.

Borrowed Money: if someone lends you $20, would you consider that as income? Personally, I wouldn't as you have to pay back this money. Similarly, if you go out and get a credit card with a $1000 limit then you haven't gained $1000 as whatever you spend has to be paid back. You could consider borrowed money as an expense or an income (basically you're adding a zero overall) but be consistent in your choice.

Impulse Spending: when budgeting, it helps to have an idea of how loose you are with your money as this will help you better set limits and manage your money. For example, when you go grocery shopping do you go by a list or just pick things out on impulse? Using a list can help you control your spending.

Diligence: accounting is largely a matter of diligence, detail, and accuracy. You don't need to know complex mathematics for this.

What Girls & Guys Said

Opinion

0Opinion

Share the first opinion in your gender

and earn 1 more Xper point!