Girl's Behavior

Girl's Behavior  Guy's Behavior

Guy's Behavior  Flirting

Flirting  Dating

Dating  Relationships

Relationships  Fashion & Beauty

Fashion & Beauty  Health & Fitness

Health & Fitness  Marriage & Weddings

Marriage & Weddings  Shopping & Gifts

Shopping & Gifts  Technology & Internet

Technology & Internet  Break Up & Divorce

Break Up & Divorce  Education & Career

Education & Career  Entertainment & Arts

Entertainment & Arts  Family & Friends

Family & Friends  Food & Beverage

Food & Beverage  Hobbies & Leisure

Hobbies & Leisure  Other

Other  Religion & Spirituality

Religion & Spirituality  Society & Politics

Society & Politics  Sports

Sports  Travel

Travel  Trending & News

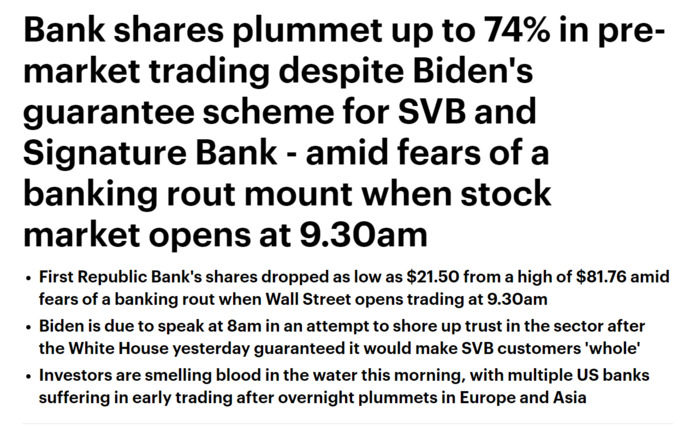

Trending & News They’ve already done the bailout. Yes, they will print money like mad. The US is in a bind now because treasury bond auctions are going badly whenever the dollar is strengthening. This means the USG will have to choose between the ability to raise debt and spend vs. the value of the dollar. I’m 100% certain they won’t allow their ability to spend like mad to be reduced, but will sacrifice the currency instead. Ultimately, the dollar will decline such that the ability of the regime to fund a huge military will be compromised, but we’re a ways off from that.

But.. They are not using printed money to pay for that. They are using what is basically a bank insurance fund that exists specifically for covering when banks can't pay out.

So yeah.. Using the backup systems to protect people to actually protect people when the time comes. Totally a radical idea apparently. And again, the money already existed for this exact type of disaster so no point printing more.

Do you republicans ever get tired of being wrong?

Soteris, being the genius leftist you are, can you explain to us up to what amount this "bank insurance fund" covers deposits? And can you explain to use what happens to deposits in excess of the amount the fund covers? Furthermore, can you explain to us how the US government would cover deposits not covered by the fund?

@Avicenna Why certainly. So, this comes from the Federal Deposit Insurance Corporation of FDIC for short. Broadly speaking it is tasked with restoring the trust in the banking system after the great depression so it is tasked with a large number of things that I will not go into detail here. What is relevant for our conversation is that it offers insurance to most banks that covers deposits up-to 250k dollars and some other limits and rules for trusts and whatever.

Point is, they offer insurance to bank customers as an extension of the Federal government to prevent bank crashes and runs and they have appropriately deep pockets to accomplish this. Problem with the recent bank runs is that most of the customers, especially small businesses, has amounts exceeding the normal amount for insurance but this is where the government stepped in and made an exception to cover everyone regardless to try stabilize the situation.

More specifically, it was the treasury department that reclassified the two banks and gave them the authority to cover customers outside of the normal 250k cap. There are of course much more happening but again, overly complicated and neither interesting nor truly relevant.

I see. I have some further questions.

-What were these two banks "reclassified" to?

- The banks (and ultimately their customers) pay the FDIC insurance premiums. These premiums are priced to cover deposits up to 250K. Where does the money come from to cover all deposits, and what is the dollar amount of the additional deposits that have now been guaranteed? Have the FDIC premiums been raised to cover the guarantee of all deposits?

-Have all bank deposits ever been guaranteed before in US history? What was the dollar value of this guarantee at that time and how would it have been funded had it been necessary to actually make all depositors whole in the event of a mass bank collapse?

-How much is the current value of the US national debt and this current fiscal year's budget deficit? How exactly would the US government cover all of these deposits?

-Do you know what moral hazard is? What caused these two banks to fail?

@Avicenna Not entirely sure what the term is called but something along the line of being a systematic risk which gives them the ability to shut down the bank and take over its assets and parts which then allows them to create a new entity to service the customers and pay out the money that are not insured.

As for the money, it comes from FDICs insurance but you are making a mistake here. The FDIC insurance is only intended to cover deposits up to 250k during normal times but it also accounts for having to step up and cover beyond that during times of economic problems which is why the premiums is a lot higher than the would need to just cover up to 250k which allows them to build up a buffer to use when they need to step up later.

As I said originally, this program was started as a result of the great depression and only insures some banks and with a limit during normal times. Its main job however is to prevent an economic event such as the great depression from hitting average people so they will naturally assume more power and control when they need to so that they can avert such situations in the future.

@Avicenna

FDIC is not funded by the federal government and is in charge of collecting its own operational costs from insurance dues. As such its not part of the deficit either by taking money or by giving money.

I know what moral hazard is. Not sure about the story about the silver bank but the Silicone Bank was screwed mostly because of its small business customers. Namely that they put in a large amount of cash without taking out many loans. Because the bank needs to invest it somewhere to provide its customers with a rate of growth on their bank deposits they are forced to put it into some form of risky investment to give a good return to both cover their customers but also their own profits.

With few options Silicone bank made the wrong choice and got wrecked by the government changing its rates and by then it was not much they could do. They were done in by bad luck and a bad business choice of targeting small business customers without a better way to guarantee profits. If you want to call having a bad business plan as "moral hazard" then fine by me.

So let me get this right, Silicon Valley Bank put its depositors' money into "risky investments". What exactly were these "risky investments" and how was it that Silicon Valley Bank could not do anything about these investments once "the government changed their rates"? Is that something a bank should do, putting its money in risky investments? Don't banks have Risk Management Departments that model changes in interest rates and other things that would affect what you term "risky investments"?

Incidentally, you seem to have a strange idea of who actually had their money in SVB:

www.npr.org/.../silicon-valley-bank-collapse-failure-fdic-regulators-run-on-bank

I see that you have been unable to answer my other questions and are trying to make other claims. Do you claim that FDIC insurance premiums can cover ALL bank deposits in the US, including ones in excess of what by law they now cover (the 250k per depositor per account?).

As a reminder, here's what you said above:

"Point is, they offer insurance to bank customers as an extension of the Federal government to prevent bank crashes and runs and they have appropriately deep pockets to accomplish this. Problem with the recent bank runs is that most of the customers, especially small businesses, has amounts exceeding the normal amount for insurance but this is where the government stepped in and made an exception to cover everyone regardless to try stabilize the situation."

@Avicenna They invested into government securities and bonds and it was risky because the government raised the interest rates making them OTM. Because customers started to demand their money back the banks were forced to sell at a loss and this spiraled into them going bankrupt since the customers in question had a much higher proportion of capital than normal bank customers due to them being mostly small businesses and therefore them demanding their money back hit much harder.

And again, normally a bank would have much more options for making money to pay for the rate of return customers are expecting but when you are mostly aiming at small businesses that is full of capital and not taking out any loans with you then you are limiting your income and maximizing your costs which forces you to invest into higher risk investments to achieve enough potential gain to make it all work.

SVB was a bank specifically aimed at startup companies AKA small businesses.

Can FDIC cover all bank deposits in USA? No. Can they cover more than the 250k limit? Yes, and by design. FDIC is not really there to protect your 250k deposit but there to prevent the next economic disaster coming from the banking sector. The 250k deposit insurance is just a bonus for the actual purpose of that money which is to be used in situations exactly like this.

Perhaps the politicians wanted to be nice to include the 250k insurance but personally I am of the opinion that if people did not see a tangible immediate benefit to the government stacking a big pile of rainy day funds then they would become upset and demand them to stop saving and use it instead because people have no concept of being prepared for the worst case scenario. Hence the 250k deposit insurance is a shield for the rainy day fund.

Again, you have a strange idea as to what constitutes a small business. And modern finance is built around the idea that US Treasurys are risk-free (for example, insurance companies put their reserves into them), in large part because of the liquidity of the market for them. So where else could SVB have put their money and not run afoul of bank regulators? And if US Treasurys were that risky, imagine what sorts of other risks banks were taking. Hence why there is concern about systemic risk that would require taxpayer money for bailouts.

The uninsured depositors were made whole because they were donors to the Democratic Party- note the Treasury Secretary said uninsured depositors would only get their money back with her approval (among others), further heightening concerns about systemic risks and bailouts that taxpayers would be on the hook for due to moral hazard.

As you have admitted, FDIC can't cover all bank deposits and wasn't designed to. It's also clear that ordinary people need to have that sort of protection because they don't have the ability or the time to determine which banks are safe for them to bank with. But to sit here and say that there's nothing to worry about when an asset class as ubiquitous as US Treasurys is causing a bank failure is naive, as is claiming that there could never be a huge bailout of large banks (ever heard the term "too big to fail"?). And you lived through the 2008 banking crisis, so you know better.

@Avicenna Its not normal treasury bonds. Those does not give enough growth which is why I have repeatedly mentioned that their customers unusually large account balances worked against the bank because that forced them to look for riskier bonds with a higher rate of return.

Other banks have smaller customers that take more loans which means they dont need as high of a return and the loans gives them a less risky method of investing their money making it significantly easier for them.

I also have no idea about what nonsense you are talking about regarding uninsured depositors. As far as I have heard, every depositor in said bank will have their deposit covered and it has nothing to do with any sort of approval. This is also, as I have said previously, not coming out of taxes so what does tax payers have to do with any of it?

Lastly, I heard that the investors and leadership of said banks were going to get shafted so I am not sure why you are bringing up moral hazard either. If anything, this is exactly what should happen. The banks get fucked but does not come back to hurt regular people.

Also, what makes you think that treasury bonds are just free money? Obviously there is a risk, especially in regards to how much the growth will be. These banks relied on getting a high rate of return. If the interest rate increased and lowered their rate of return by just a bit then they would go from profitable to unprofitable in a heartbeat. Does not take much to make a big difference and then you add the fact that financial advisors caused a bank run by telling their customers to pull their money which literally no bank can survive and thus it becomes a self fulfilling prophecy where the banks have unusually low reserves thanks to bad investments and people being told to remove their investments. A devastating one-two combo.

Not saying that there would never be a bank bailout, but this ain't it so far and you are just letting your political bias contradict fact.

You clearly lack the background to understand the issues here. Everyone also knows that you are a deluded and arrogant leftist, so it's obvious who is biased here.

Where did I say Treasury bonds are "just free money?". I didn't, and your lack of understanding led you to say something dumb like that. And you are too dumb to realize that the deposits in SVB over 250k getting protected required approval by the FDIC board, the Federal Reserve Board, and the Treasury Secretary

"A bank only gets that treatment," she told U. S. Republican Senator James Lankford, if supermajorities of the boards of the Federal Reserve, the Federal Deposit Insurance Corp and "I, in consultation with the president, determine that the failure to protect uninsured depositors would create systemic risk and significant economic and financial consequences."

www.reuters.com/.../

"Uninsured deposits" are ones over 250k. Contrary to your false claims that these were ordinary people, it was in fact sophisticated businesspeople and companies who knew their deposits were uninsured.

The market for shorter-duration Treasurys is liquid enough and high-yielding enough that SVB could have invested there rather than in longer durations.

@Avicenna I am just extrapolating from what you said. Namely that " But to sit here and say that there's nothing to worry about when an asset class as ubiquitous as US Treasurys is causing a bank failure is naive" which is stupid and already disproved several times ever since I started to explain this. Basically, you refuse to listen which is further hammered home with you continuing to talk about tax payers and bank bailouts and moral hazards which objectively does not apply to this situation but that you continue to try shoehorn in again and again even after I explicitly tell you they are irrelevant.

Why? Because you never cared about anything I said or any proof on my side. You had your view of this situation already and reality was never going to change your mind because what you believed in was politically beneficial for you.

Also, I believe in an equal society, that means that "sophisticated business-people" are not from another class than "people" as if we are living in a caste system or whatever. Also, SVB could have done a million different things but that just a question of hindsight. They did what they thought was best for them and they miscalculated. End of story.

Opinion

10Opinion

The short term goal here is to eliminate multiple smaller banks and condense what's left into a handful of larger ones (probably four or five). The long term goal is federalization of the entire banking system, most likely through a digital dollar.

Yes and with an accompanying 16% interest rate, hyperinflation, deflation, and both War and continued pharma build-up.

It may be the last ditch effort to save the economy but it won't work. In less than three short years the democrats have managed to tank the world's greatest economy.

I blame the left and Biden for the shit storm we are in. It's not just two banks now, it's a total of 5.. This is what you get when you support leftist policies and the like.

Any self-awareness from the lefties on how bad they fucked up?

Why the Hillary gif when you're bitching about Biden? She doesn't even run for election anymore.

The damage bush and trump did is always fixed by a democrat.

Funny, Trump loosened the regulations. And you blame Dems. Typical.

This is an example of the CCP propaganda Odd has been echoing: www.bloomberg.com/.../china-blames-us-bank-woes-on-bad-regulation-political-bickering

Now, Odd, you are a known worshipper of the CCP. You recently said that the US "needs China"., but when asked to explain why, you had no answer.

But answer the questions I posed to you above. Exactly what was changed under the Trump Administration that caused Silicon Valley Bank to go belly up? Are you sure it wasn't something else that caused the bank to collapse? After all, it was only SVB and one other bank that went under, so why would you assume it's some vague rule change you can't even detail, much less explain. You might want to look at these articles before you continue to make a fool of yourself:

www.npr.org/.../silicon-valley-bank-collapse-failure-fdic-regulators-run-on-bank

news.bloomberglaw.com/.../fed-alarms-at-svb-began-more-than-year-ago-as-examiners-changed

@Avicenna I’ve answered you may just not have understood. If we like iPhones at current prices we need cheap Chinese labor. I don’t much prefer children assembling iPhones in China and consider the country belligerent and dictatorial.

But your low IQ makes it tough for us to discuss multi faceted issues. So…who’s my good boy! You my good boy! Yes you is!

You didn't answer previously, but now that you have, you have proven yourself to be dumber than a pile of rocks. You think that child labor in China (a country that also uses slave labor) is a necessity. It's quite possible to make iPhones in Vietnam, India or elsewhere where labor is now less expensive than China rather than relying on our biggest enemy. And we could re-shore some of their production to the US as well as relocating some to Mexico if we wanted to. Would we pay more for them if made in North America? Sure, but Chinese-made products' retail prices are a lot higher than the differential in labor rates, so who's really benefiting? Not the consumer.

But even that single issue is too multifaceted for you. And you are still unable to back up your mindless claims about the SVB failure. Again, too multifaceted for a CCP stooge like yourself.

-Labor is cheaper than China in some other Asian countries

-We should not be buying the product of slave labor

-Who said anything about invading China? Are you drunk?

All we have to do is kick out the CCP spies and re-shore our manufacturing base or move it to countries like Vietnam, India, Indonesia, or the Philippines. No need to invade (if that were even possible).

I don't think they'd be three times the price, and even if they were that expensive if made in the US, we could make them in less expensive places outside of China.

Odd, you're too young to remember the Soviet Union, which today's China has a lot of similarities to. No one was talking about invading it and hardcore leftists in fact had a hard on for the place. Other strategies were used to deal with the Soviets, including not allowing them to entrap our NATO allies in trade like China does.

I dont think your iPhone will be 10 times the price. Apple like an employer will pay as little as they can. China's big thing for years was always the availability of cheap labor, but with more automation it becomes less important. Its kinda like what happened with most of the dock working jobs after ww2, these armies of people to unload cargo ships were no longer needed when ship containers were being used. On a side note conditions are so bad in Chinese apple factories that they had to put nets up around the buildings because workers kept jumping off the roofs

Different situation completely, dumbass!

You mean, they haven't, already?

Be the first girl to share an opinion

and earn 3 more Xper points!

You can also add your opinion below!